The US-China trade war since 2018 had led many companies with operations in the US to shift parts of their manufacturing either back to the US or Mexico or to emerging markets in South and South East Asia countries. As a result of this, while the total imports of all goods in the US decreased from $2.61tn in 2018 to $2.57tn in 2019, imports from China to the US decreased drastically from $562.3bn $472.5bn during the same period.

This was compensated mostly by imports from Mexico, as well as imports from most of the South and South East Asian countries. US imports increased from most of the South and South East Asian nations, with notable increases from Vietnam, from $51.3bn to $69.4bn, Taiwan ($47.3bn to $56bn), Cambodia ($4.0bn to $5.6bn), and India ($56.4bn to $59.9bn).

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The Covid-19 outbreak is likely to further accelerate this process, with companies not only in the US, but also from Western Europe as well as from South Korea and Japan, looking to diversify their production and reduce their overdependence on Chinese production. This has been necessitated as supply chain disruptions due to the lockdown in China disrupted operations across the world leading to production stoppage in countries that were not affected by the virus outbreak.

For example, the lockdown in Wuhan, which is a major supplier of automobile parts to companies across the world, disrupted automobile production across the world and led to temporary shutdowns in the US, South Korea and Japan in February even when the virus outbreak had been limited mostly to China. Similarly, electronics manufacturers, including smartphone makers, faced supply disruptions.

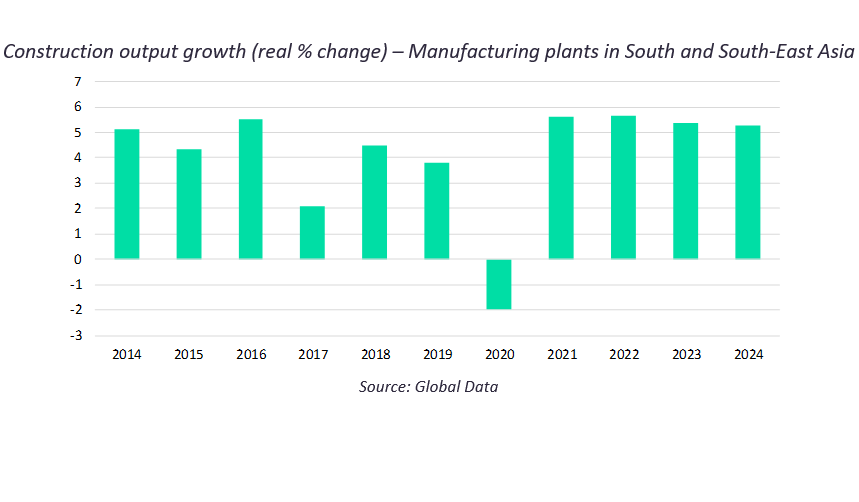

Growth in the construction output value associated with manufacturing plants in South and South East Asia is forecast to drop in 2020, reflecting the major disruption caused by Covid-19. The current forecast is for a drop of close to 2%. However, in the event that demand shifts to production in these markets and away from China, there is scope for a solid recovery in investment in new manufacturing production capacity after the global pandemic is contained.

Governments, as well as large manufacturers, across the world are seriously pondering plans to reduce their over-dependence on Chinese production. The Japanese Government became the first to take steps in this direction, by announcing a $2.2bn assistance to domestic companies to shift production from China. The assistance, which is a part of the country’s $1tn economic stimulus package, earmarks $2bn funds for companies shifting production back to Japan, with the remaining $200m meant for companies shifting their production to other countries.

Although no other country has so far followed the Japanese Government’s idea of explicitly announcing financial assistance to companies, but the increasing geopolitical tension between China and the Western world is likely to hasten this trend. This reflects accusations that the Chinese Government has lacked transparency in reports regarding the origin of coronavirus outbreak, as well as the export of sub-standard and faulty medical equipment and testing kits.

Vietnam and India potential have the most to gain. Even before the outbreak of Covid-19, many companies had been shifting their production base to Vietnam. Although the above-average export growth in 2019 was not entirely a direct result of the shifting of production from China, as many Chinese producers shipped their goods to the US by first rerouting it from Vietnam, but the country has been emerging as the new manufacturing hub for furniture, footwear, readymade garments and other linked industries.

Even large Chinese companies such as TCL, a major television manufacturer, has shifted its base to Vietnam. This has been helped by the availability of cheap labour, as well as the government’s plan to build new industrial zones with an aim to increase industrial production. Under the industrial development strategy 2025, the Vietnamese Government aims to increase the share of industrial production in the country’s total export value from 80% in 2015 to 90% by 2025.

India provides a unique opportunity to companies relocating from China as it not only provides cheap labour but also a vast captive market, with the world’s second-largest population and an ever-expanding middle class.

The Indian Government’s decision to reduce effective corporate taxes in 2019 to 25.17% and a special corporate tax rate of 17.01% for new investments between October 2019 to 2023 is also likely to make the country attractive to manufacturers looking to shift production. In order to attract investments into the electronics segment, in March 2020, the Indian Government announced three schemes with a total outlay of Rs480bn ($6.5bn) including a five-year Production Linked Incentive (PLI) scheme that will provide 4%-6% incentive to companies for manufacturing from India.