Construction investment activities that had started picking up in March in China show a further uptick in April, with the latest data showing further progress in investments in both fixed assets and real estate segments. Although the cumulative four months’ data until April still shows a huge year on year contraction due to the lockdown and containment measures during the first two months of the year, but the growth in April has further reduced the accumulated contraction rate for the year.

Total accumulated investment in real estate development improved from a decline by 7.7% year on year in the first three months to a drop of 3.3% in January-April. This was due to a pick-up in activities in April with growth of 7%, which followed marginal growth of 1.1% in March and a 16.3% contraction during the first two months. The investment in residential buildings increased by 7.2% in April, following growth of 1.8% in March, with the cumulative investment in January-April still down at -2.8%. While investments in office buildings increased by 11.0% in April, it still showed a higher cumulative contraction of 4.8% in the first four months.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Similarly, the decline in investments in fixed assets improved from a contraction of 24.5% in January-February to 16.1% in January-March and further to 10.3% in January-April. In terms of month on month growth rates, investment in fixed assets increased by 6.2% in April, following a growth of 6.1% in March and a contraction of 20% in February. This was because by mid-March, the country had restarted construction thousands of key construction projects outside of Hubei province. By 15 March, construction work on major rail infrastructure had gradually been stimulated, with construction works resuming on 108 major rail construction projects across China, representing 93% of the country’s railway projects under construction.

To support the ongoing recovery, the Chinese government has accelerated the launch of new projects. According to the National Bureau of Statistics, the country had 22,693 projects at the end of April, of which 5,614 projects are large projects (those valued at more than CNY100m). The total number of projects reflects an increase of 10,695 projects in the month of April. The focus on new projects can be gauged from the fact that total investment on newly-launched projects increased by 1.1% y-o-y in January-April 2020.

Meanwhile, the government has announced intentions to increase the scale of local government special bonds to mitigate the impact of COVID-19 on the economy. These bonds have traditionally been used for infrastructure investments. Li Keqiang, the Chinese Prime Minister announced that the government plans to increase the issuance of local government special bonds this year by about 75%, from CNY2.15tn in 2019 to CNY3.75tn in 2020. In April, local governments issued special bonds worth CNY120 billion, taking the cumulative year total to CNY1.22tn, while general bonds worth CNY166.8bn were also issued in the month, taking the cumulative total at the end of April to CNY673.3bn. New bonds accounted for 41.9% of the CNY286.8bn bonds issued in April, with the rest comprising refinancing bonds.

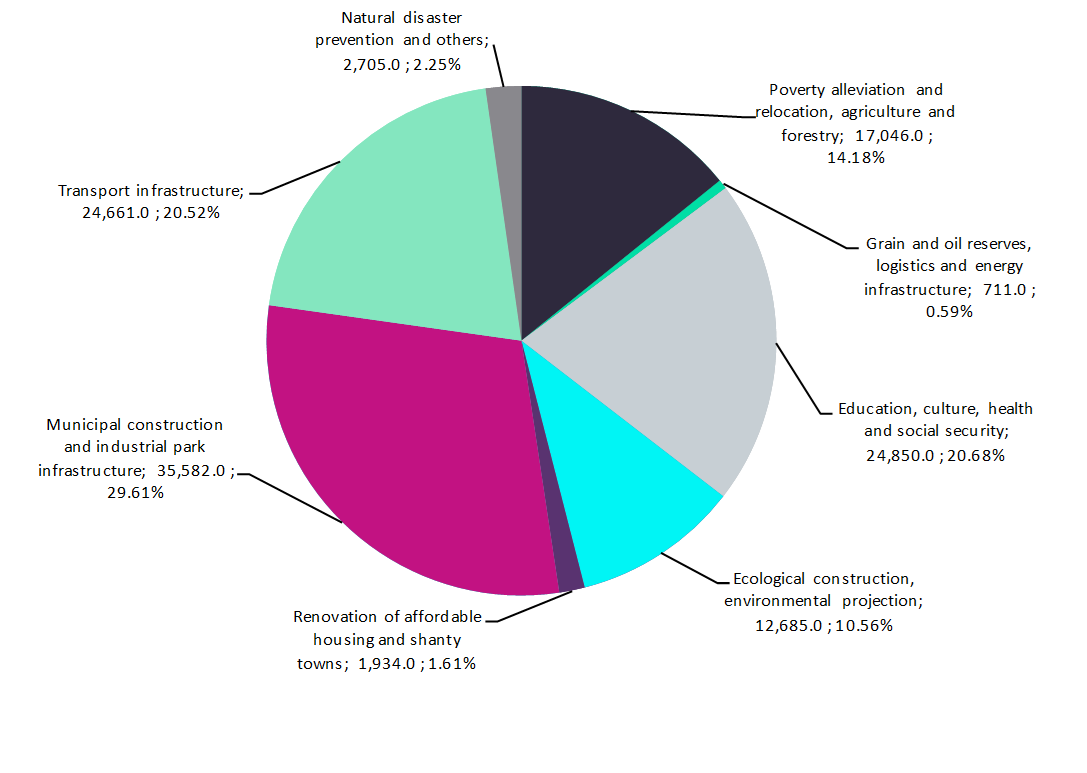

In terms of investments of the capital from the new bonds issued in April, municipal construction and industrial park infrastructure accounts for the largest share – 29.6%, followed by Education, culture, health and social security with 20.7% and transport infrastructure with 20.5%.

Apart from special bonds, the Chinese government is also trying to look at alternative sources of investments and has approved a pilot scheme for real-estate investment trusts (REIT). The scheme, announced on 30th April by the China Securities Regulatory Commission and the National Development and Reform Commission (NDRC), stipulates that the REITs would be listed on the Shanghai and Shenzhen exchanges and would cover capital-intensive infrastructure assets including urban utilities, airports, data centres, warehouses, sewage treatment facilities, toll roads, high-tech industrial parks and telecom and information networks. The pilot scheme is expected to be launched during the second half of 2020 and would be limited to infrastructure investments in key areas: the Xiong’an economic zone, Beijing-Tianjin-Hebei region, Yangtze River Delta and the economic zone along the river, the Hong Kong-Zhuhai-Macao area and Hainan province.