For much of the post-pandemic period, the office sector has been treated as construction’s awkward problem child. Hybrid work cast doubt on demand, valuations swung unpredictably and lenders grew cautious. For developers, new projects suddenly carried far more risk.

The latest pipeline data complicates that narrative.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

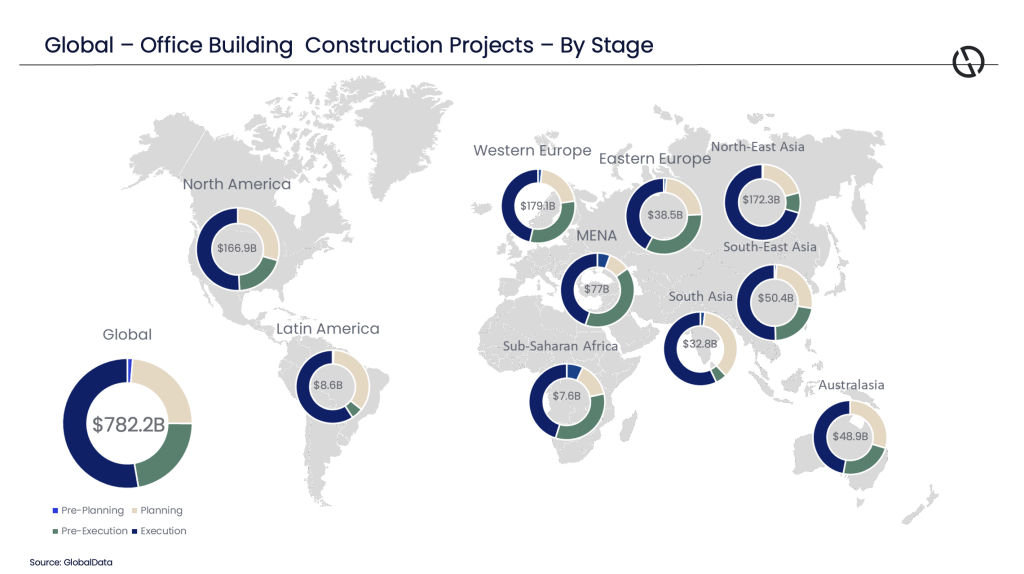

GlobalData is currently tracking office projects worth $782.2bn worldwide in its ‘Project Insight – Global Office Buildings Construction Projects’ report for Q1 2026. Crucially, 75.4% of that total ($589.9bn) has already reached pre-execution or execution stages, with 24.6% ($192.3bn) in earlier planning phases.

That distinction matters. Much of the capital tied up in this pipeline is no longer speculative. Projects at pre-execution typically have funding structures in place, planning approvals secured and tenant strategies defined. In other words, they are moving.

For contractors and suppliers in global construction, the signal is clear enough: the office market has not collapsed. But it has become far more selective.

Schemes progressing today tend to share similar characteristics. They have stronger pre-letting strategies, clearer financing and a far more prominent sustainability narrative than was common a decade ago. The market is not returning to the old ‘build it and they will come’ cycle. Instead, it appears to be entering a more disciplined phase in which quality and adaptability determine which buildings get built – and which quietly become obsolete.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataA fragmented global market

The regional distribution of projects reinforces the point that there is no single “office market”.

Western Europe accounts for 22.9% of the pipeline, narrowly ahead of North-East Asia (22%) and North America (21.3%). The Middle East and North Africa holds 9.8%, while South-East Asia represents 6.4%.

For international contractors, this spread suggests opportunity across both mature and growth markets. But the drivers differ significantly.

In Western Europe, for example, the scale of the pipeline is closely linked to the region’s aggressive decarbonisation agenda and its ageing office stock. Many buildings constructed during earlier development cycles now struggle to meet tightening energy standards without significant upgrades. That is pushing landlords towards deep refurbishments and redevelopment rather than simple refurbishment cycles.

The spending trajectory also suggests the market is regaining momentum. (Although this may be affected by geopolitical conflicts.) GlobalData expects annual office construction expenditure to rise from $103.1bn in 2025 to $136.9bn in 2026, reaching $150.1bn by 2027, assuming projects proceed as scheduled.

Even allowing for delays – a routine feature of construction programmes – the direction is unmistakable.

What remains less certain is whether this represents a cyclical recovery or a structural shift in what offices are expected to provide.

Return-to-office politics meets hybrid reality

One factor shaping the current cycle is the renewed push for in-person work.

GlobalData notes a growing trend among large corporates to mandate office attendance as part of workplace “normalisation”. Technology and media groups including Apple, Meta, Disney, Amazon and X have all introduced structured return-to-office policies.

Governments are also weighing in. In January 2025, US President Donald Trump directed federal departments and agencies to end remote work arrangements and require full-time in-person attendance.

For the construction sector, these policies function less as cultural statements than as demand signals. Stronger attendance expectations can shift boardroom decisions from pause to proceed when it comes to refurbishments, new fit-outs and, occasionally, entirely new developments.

Yet it would be misleading to treat this as a simple return to pre-2020 working patterns.

Hybrid work has not disappeared; it has settled into a more stable form. Many organisations now operate with flexible attendance expectations, producing a different utilisation pattern: busy mid-week peaks and quieter Mondays and Fridays.

That shift is reshaping design briefs.

Offices optimised purely for desk density are gradually giving way to buildings designed around collaboration, meetings and client engagement. Employers increasingly want spaces that justify the commute. That means better amenities, stronger digital infrastructure and environments that resemble hospitality venues as much as traditional workplaces.

For construction teams, delivering those spaces requires higher servicing levels, stronger acoustic performance and greater technological integration – often within tight programmes and live operational buildings.

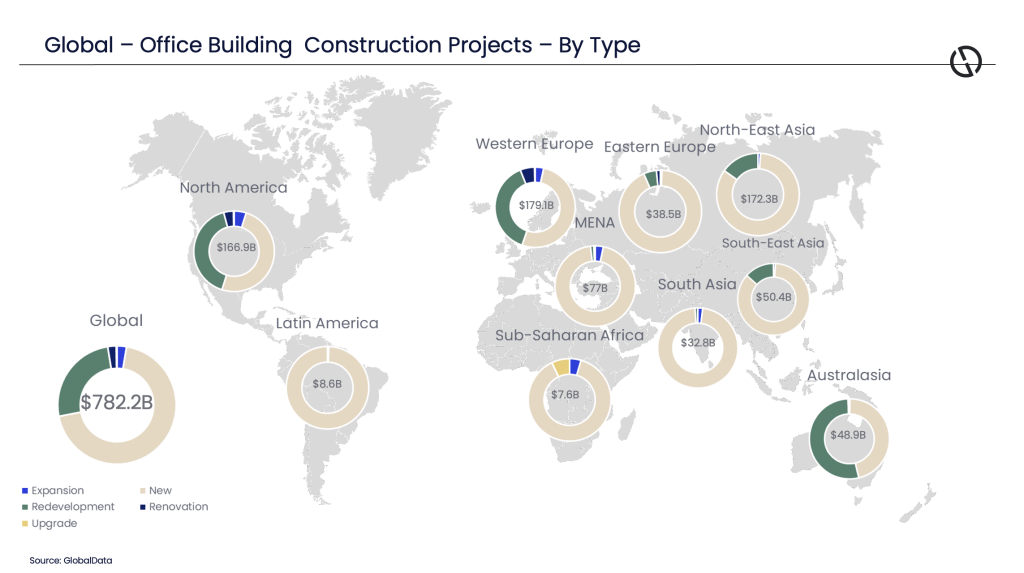

Retrofit becomes central to the office market

The biggest shift may lie not in new towers but in existing stock.

Refurbishment and CAT A-plus upgrades are becoming strategically as important as new construction. In many cases, the ‘value-add’ office is created through transformation rather than ground-up development.

That typically involves extensive interventions: facade upgrades, mechanical and electrical replacement, smart-building systems and measures to reduce operational carbon.

For contractors, the implication is clear. Expertise in complex retrofit projects – particularly those delivered in occupied buildings – is becoming a major competitive advantage.

Landlords face growing pressure to modernise assets that would otherwise struggle to attract tenants or financing. The result is a market in which technically demanding refurbishment projects may become as common as headline-grabbing skyscrapers.

Offices within broader urban regeneration

Another stabilising factor for the sector is government investment in urban infrastructure.

Transport upgrades and regeneration programmes often support higher-density development in central districts. But offices are increasingly part of mixed-use developments, rather than stand-alone speculative blocks.

That introduces both opportunity and constraint.

Residential, life sciences and logistics developments often compete for the same land and capital, sometimes offering more predictable demand. Planning authorities are therefore more likely to support office space where it demonstrably contributes to broader economic or transport objectives.

In practice, this means more schemes where offices sit alongside housing, retail and leisure uses, with construction programmes shaped by the phasing of large regeneration sites.

For contractors, these projects bring greater logistical complexity. Managing interfaces between multiple building types and coordinating with public-realm works requires careful planning – and often earlier contractor involvement in the development process.

Flexible offices reshape fit-out demand

Hybrid working has also accelerated demand for flexible offices, serviced workplaces and co-working hubs.

For occupiers, the attraction is scalability: shorter leases, adaptable layouts and shared amenities.

For the construction supply chain, flexible space introduces a different operational logic. Buildings must tolerate frequent reconfiguration and higher tenant churn. Designers increasingly favour modular components, from demountable partitions to adaptable mechanical systems.

Fit-out cycles are also becoming faster and more repetitive.

Contractors capable of standardising elements of delivery and supporting portfolio-wide roll-outs may therefore find themselves at an advantage. Those reliant on bespoke design for every project may struggle to maintain margins in an increasingly speed-focused market.

Sustainability as the new investment filter

Perhaps the most significant shift in office construction lies in sustainability.

“Green buildings” were once a marketing distinction. In many markets, they are now a baseline requirement.

Assets unable to meet tightening energy standards increasingly face weaker tenant demand and a shrinking pool of investors. That reality is already influencing construction scopes: deeper electrification strategies, facade retrofits, heat-pump installations and closer scrutiny of embodied carbon in materials.

For contractors, sustainability has become both a technical and commercial competency.

Clients now expect credible carbon reporting, supply-chain transparency and evidence that operational targets can be achieved in practice, not merely predicted during design.

This is gradually pushing the industry towards performance-based delivery models, where commissioning, operational testing and post-occupancy evaluation form part of the construction process itself.

Capital returns – cautiously

Despite the uncertainty that has surrounded offices in recent years, capital is beginning to return to the sector.

GlobalData cites $1.6bn in financing announced in January 2026 by a consortium including Bank of America to support US office construction through 2028. The report also highlights a $2bn mixed-use project at 633 North Orange Avenue, alongside JPMorganChase’s planned 278,709m² headquarters development at Canary Wharf in London.

The significance of these projects lies less in their individual details than in what they reveal about investor behaviour.

Financing remains available, but it clusters around schemes with scale, strong sponsors and clear long-term demand. Lenders increasingly prioritise delivery certainty and assets capable of meeting future regulatory requirements.

This creates a more polarised market. Flagship developments and best-in-class refurbishments can still attract capital. Secondary assets without credible upgrade strategies risk falling rapidly out of favour.

A different kind of office boom

Taken together, the data suggests the office sector is not disappearing – but it is changing.

Construction activity appears likely to expand over the next few years, supported by infrastructure investment, evolving workplace policies and the need to modernise ageing building stock. Yet the projects that proceed will look different from those of previous cycles.

Hybrid work is reshaping building layouts. Sustainability requirements are tightening design constraints. And a growing share of investment is directed towards upgrading existing assets rather than expanding supply.

For the construction industry, the message is straightforward enough.

The next phase of office development will not reward those who simply build the fastest. It will reward those able to combine retrofit expertise, carbon literacy, digital delivery and operational performance into buildings that tenants – and regulators – are prepared to support.

The pipeline suggests offices will continue to be built.

The question is whether the industry is ready to build the kind that the market now demands.

Extracted and interpreted from a GlobalData report and project pipeline monitoring data. Figures and examples cited are attributed to GlobalData’s office building project pipeline insights.

To access the full report, visit the GlobalData Construction Intelligence Centre: www.globaldata.com/industries/construction.