The global construction outlook for 2026 isn’t just cooling off. It’s reshuffling the deck.

As we move further into 2026, growth hasn’t collapsed, but it has thinned out and shifted shape. Some regions are still expanding. Others are stalling. And across the board, contractors are working harder for thinner margins.

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

What’s behind it? Three big forces: tighter credit, more protectionist trade policy (particularly from the US), and a labour market that simply doesn’t have enough skilled people. Add in supply chains that still haven’t fully settled, and you get a market that feels tougher than the headline growth numbers suggest.

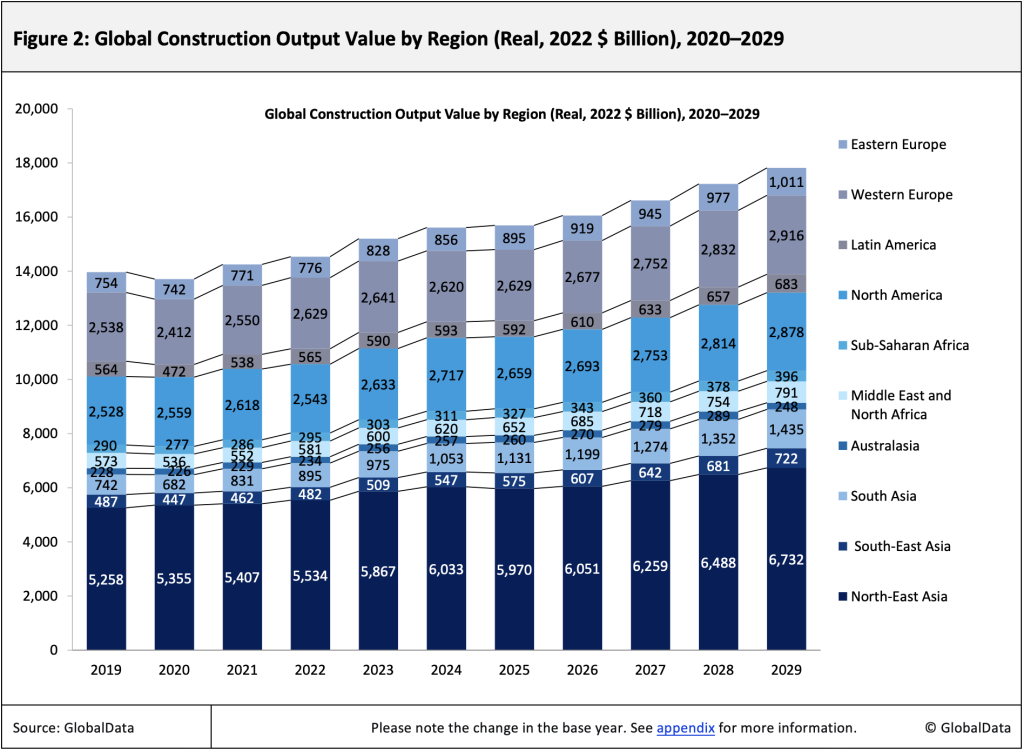

GlobalData estimates global construction output grew just 0.5% in real terms in 2025. On paper, that’s modest but positive.

In practice? It feels harsher.

Trade friction hasn’t disappeared; it’s become a permanent line in the cost plan. Tariffs and cross-border levies don’t just raise prices; they force companies to reroute supply chains. That takes time. It adds duplication. And it keeps materials costs stubbornly high, even when demand cools.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataFinancing is the bigger pressure point For 2026’s global construction outlook . Elevated interest rates across developed markets have hit project viability hard. Residential feels it most sharply, but commercial and industrial projects aren’t immune. Even when capital is available, it comes with tighter conditions and higher costs.

We’re seeing the knock-on effects everywhere: delayed starts, redesigned schemes, thinner contingency, more aggressive risk transfer. Cashflow management now separates firms that endure from firms that disappear.

And then there’s labour.

Skills shortages haven’t eased. In parts of Europe and North America, labour immobility and demographic pressure have pushed up wages and extended delivery schedules. Insolvencies are rising. Cost inflation may be stabilising, but that’s not the same as relief. Many contractors are still working through legacy contracts priced before wage escalation and supply-chain disruption were fully understood.

Stability, in other words, doesn’t mean comfort.

Growth is no longer synchronised

One of the clearest signals in GlobalData’s outlook is divergence.

North America shrunk by 2.1% in 2025. North-East Asia and Latin America were also expected to decline. Meanwhile, South Asia, South-East Asia and the Middle East and North Africa were each forecast to grow by more than 5%.

That split changes behaviour.

If you’re an international contractor, where do you place your bets? Mature markets offer familiar procurement models and clearer legal frameworks, but flatter pipelines. Growth markets offer momentum and government-backed infrastructure, but bring currency, political and delivery risk.

Suppliers face a different puzzle. When demand swings between policy-driven infrastructure and subdued private development, capacity planning gets messy. You can’t simply extrapolate from last year’s order book anymore.

Residential weakens, and the pain spreads

In the US and Western Europe, residential construction has taken the clearest hit.

US construction spending fell by an estimated 0.4% in 2025, with multifamily activity dropping sharply and single-family still declining. Europe saw contraction in major markets including Germany, Sweden and France.

Residential weakness rarely stays contained.

It moves quickly through smaller contractors, specialist trades and distributors who depend on volume. When insolvencies tick up, subcontractor capacity becomes unstable. And even well-funded projects start to feel riskier because the supply chain underneath them is more fragile.

Main contractors now have to ask tougher questions at tender stage: Who’s pricing aggressively because they’re confident and who’s pricing aggressively because they need cash?

That distinction matters.

Infrastructure helps, but it’s not a cure-all

Public infrastructure has acted as a stabiliser in many developed markets. The EU’s Recovery and Resilience Facility, Canadian renewable and transport programmes, and Australian infrastructure initiatives have supported activity. India and Saudi Arabia continue to push strong pipelines.

But infrastructure-led markets bring complications.

As residential and commercial work soften, more contractors chase public projects. Competition intensifies. Margins compress. Bidding gets sharper – sometimes too sharp.

Infrastructure projects also carry higher interface risk and longer schedules. Utilities coordination, ground conditions, stakeholder approvals – these aren’t minor variables. Add labour scarcity and procurement delays, and small issues snowball quickly.

So yes, infrastructure can stabilise output figures. But it can still increase contractor stress if procurement models push disproportionate risk onto delivery teams.

The firms that hold up best tend to share a few traits: disciplined bid selection, strong commercial governance, and mature programme controls. Scale helps, but only if it’s paired with risk control and cash discipline.

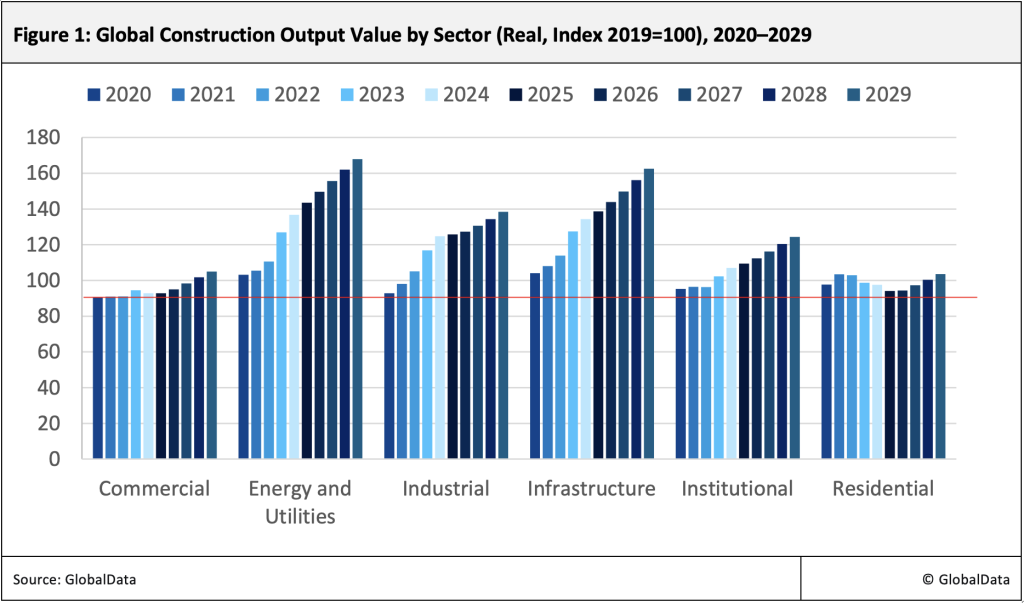

Commercial and industrial demand splits in two

Office construction remains weak in many markets. But other segments – data centres, life sciences facilities and advanced manufacturing – are driving growth.

Data centres, in particular, are reshaping demand.

They compress timelines. They concentrate spending in MEP and power-intensive scopes. They demand rigorous commissioning and supply chain coordination. And they trigger second-order works – substations, transmission upgrades, grid reinforcement, sometimes water infrastructure.

In markets where broader commercial development has slowed, these facilities keep pipelines active.

Manufacturing is more complicated. In the US, activity has stagnated despite significant industrial policy momentum. Announcements don’t always translate into groundbreakings. And even when projects proceed, long lead times for electrical equipment and specialised components introduce fresh uncertainty.

Contractors who engage early with owners and manage procurement risk carefully will convert more of these opportunities into executable work. Those who assume policy momentum guarantees delivery may be disappointed.

Energy and utilities: the most bankable long-cycle segment

If one theme dominates the outlook, it’s energy.

GlobalData identifies energy and utilities as the most promising segment. China alone is expected to invest around $13.8trn in its energy transition. Globally, renewable investment hit a record $386bn in the first half of 2025 – up 10% year-on-year.

In the US, policy emphasis has shifted somewhat, with greater attention to fossil-based and nuclear solutions to support data centres and AI infrastructure. Regardless of the mix, one fact stands out: grid capacity has become the gatekeeper of economic growth.

Power infrastructure is no longer background enabling work. It’s central.

That creates opportunity across transmission, distribution, storage and generation. But it also creates constraints. Permitting delays, electrical equipment bottlenecks and shortages of specialist labour will determine the real pace of delivery.

Money alone won’t solve those.

Insolvency risk is no longer cyclical

Here’s the uncomfortable truth: a market can grow slightly and still see rising failures.

GlobalData highlights increasing insolvencies across Europe and North America. Western Europe illustrates the paradox well – marginal growth in output, yet contractor viability weakens.

Why? Because harsh risk allocation, slow payment cycles and fixed-price exposure in a volatile cost environment squeeze balance sheets.

Insolvencies ripple outward. Clients face retendering and delays. Surviving contractors become more selective. Risk premiums rise. Long-duration projects become harder to price confidently.

Over time, this embeds caution into the system.

What this means for 2026

The regional picture for global construction outlook in 2026 reinforces a broader conclusion.

Developed markets are hovering near stagnation and leaning heavily on public and energy investment. Developing regions – particularly South Asia, South-East Asia and MENA – benefit from policy-backed infrastructure and energy commitments that provide clearer pipeline visibility.

North America illustrates volatility. Trade policy shifts feed quickly into contractor costs. Yet data centre and AI-driven infrastructure spending cushions activity. The risk? Concentrated capital crowds out other essential infrastructure while intensifying wage competition.

Western Europe looks stable in aggregate but stressed operationally. Political uncertainty and residential softness dampen private investment. Targeted national energy and transport programmes offer opportunity, but not broad-based recovery.

China’s transition away from property-led growth continues to reshape demand towards infrastructure and energy. That shift may create opportunities but it won’t fully offset weaker residential and commercial volumes.

[subhead] Discipline beats expansion

The old playbook – grow volume, rely on residential to steady the cycle, assume globalised supply chains will normalise – looks outdated.

Growth is slower. It’s more politicised. And it’s concentrated in technically demanding sectors.

In 2026, competitive advantage will likely rest on three capabilities:

- securing and retaining scarce skills

- managing procurement risk in a tariff-shaped supply chain

- protecting cashflow through disciplined contracting and client selection

Resilience isn’t just defensive anymore. It’s strategic.

And perhaps that’s the real shift. In a fragmented market, survival isn’t guaranteed, but it is manageable for firms willing to adapt, say no to the wrong work and focus on the projects that truly must be built.

This article and the global construction outlook for 2026 is based on estimates and forecasts from GlobalData’s global construction market analysis and 2025–2029 outlook (extract supplied).

To access the full report viit the GlobalData Construction Intelligence Centre: www.globaldata.com/industries/construction.