Education construction has become one of the clearest ways governments try to turn policy into something tangible. Classrooms, labs and campuses are not abstract promises; they are physical proof that a system is working. Or failing.

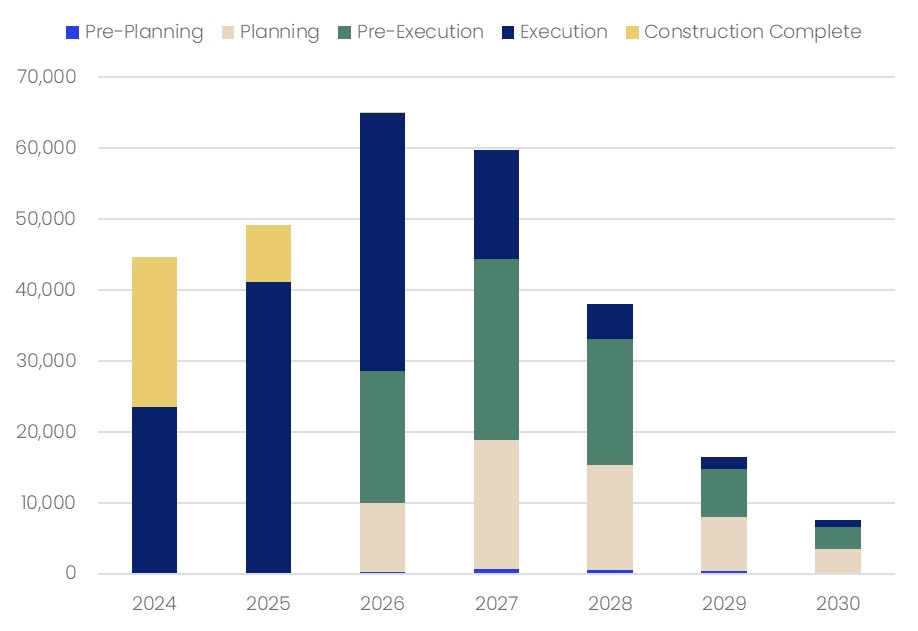

GlobalData’s tracked pipeline stands at $283.5bn. What is striking is not just the size, but the stage. Roughly four-fifths of projects sit in pre-execution or execution. That tells us something important. This is no longer about plans being debated in ministries. In many markets, schemes have moved into design finalisation, procurement and early delivery, where outcomes depend less on ambition and more on whether the industry can actually build what has been promised, as part of a selective global construction outlook.

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

The underlying demand is clear enough. Unesco’s latest SDG4 reporting puts the number of out-of-school people at around 272 million in 2023, higher than earlier estimates. That gap has sharpened political focus. Even as some governments look for savings elsewhere, education capital spending has, in several cases, been protected. Few ministers want to be seen cutting school building programmes.

For the construction sector, this creates a sizeable opportunity. It also raises the stakes. Education projects are visible, sensitive and operationally complex. They must meet safety and environmental standards, and they must open on time. A school that is late for the start of term is not just a project delay; it is a public failure.

A strong pipeline, but tight capacity

The late-stage nature of the pipeline is both reassuring and slightly unnerving. On one hand, it improves near-term revenue visibility. On the other, it compresses capacity. When most projects are approaching delivery at the same time, shortages of designers, project managers, specialist trades and compliant materials begin to show up as programme risk.

Global Education Construction Project, Projected Spending Value by Stage ($M)

Cost pressures are also harder to manage. There is less room to redesign or defer scope, so inflation tends to land with clients and contractors rather than being engineered out early. We have seen versions of this cycle before. A strong pipeline meets a constrained supply chain, and the industry quietly recalibrates expectations. The difference this time is the political sensitivity. Schools and universities are not discretionary assets. Delays attract scrutiny.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataRegional patterns reinforce that point. North America accounts for the largest share, with about $119.6bn of projects, followed by Western Europe at $72.3bn. These figures reflect not just demand, but the ability of planning and funding systems to convert policy into deliverable schemes. Markets with stable procurement frameworks and established delivery ecosystems tend to move projects through the pipeline more effectively.

Funding shapes risk and design

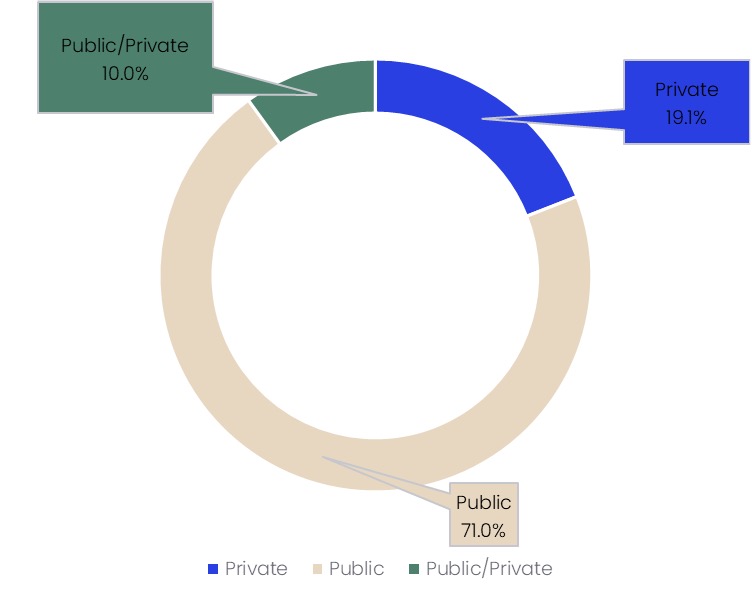

Funding structures matter more than the headline numbers suggest. Around 71% of the pipeline is publicly financed, with private funding at roughly 19% and public-private partnerships making up the balance.

Public programmes tend to favour standardised designs and repeatable delivery models. They prioritise compliance, cost control and scale. Private higher-education projects often push in a different direction, towards differentiation, research capability and mixed-use campuses that double as real estate plays.

PPPs, although smaller in share, have an influence beyond their weight. Governments use them to accelerate delivery and shift life-cycle responsibilities into long-term contracts. That changes what clients expect. It is no longer enough to complete a building; it must perform over time. For contractors and consultants, that raises the bar on operational thinking.

Politics, place and delivery reality

North America illustrates how quickly political context can affect delivery. The US pipeline is large, but implementation has been uneven in recent years due to federal funding uncertainty and policy shifts. Even where spending envelopes remain intact, procurement can stall if direction is unclear. Canada offers a steadier counterpoint, with long-term provincial programmes creating more predictable conditions.

Global Education Construction Project Pipeline, Funding Mode (% of total)

Western Europe presents a different challenge. Much of the work is not new build but renewal. Ageing estates, decarbonisation targets and safety upgrades dominate. Delivery is constrained by live environments, tight sites and complex compliance requirements. It is less about landmark projects and more about consistent execution.

Elsewhere, the picture becomes more uneven. In parts of MENA, large-scale programmes are advancing quickly, often tied to broader economic strategies (ongoing conflicts notwithstanding, of course). Speed is a priority, which favours standardisation and industrialised construction, but it also increases the need for robust quality assurance. In sub-Saharan Africa, the issue is less demand than financing. The pipeline is small relative to need, reflecting a persistent funding gap. Delivery tends to be incremental and cost-sensitive.

In Asia, the balance between public demand and private capital is more pronounced. South-East Asia’s pipeline has a strong private component, bringing faster decision-making but also a sharper focus on returns and student experience. In North East Asia, planning is becoming more data-led, with demographic trends informing where capacity is expanded. That supports more structured, repeatable delivery.

The real test: delivery, not demand

Taken together, these dynamics point to a shift in where value is created. The question is no longer whether there is demand for education infrastructure. There is. The question is whether projects can be delivered reliably, at scale, and to the standards now expected.

For contractors and consultants, that places a premium on programme certainty, cost control and operational performance. Clients are looking beyond capital cost. They want buildings that work in practice, with predictable energy use, good environmental conditions and low maintenance burdens.

It also requires firms to move between funding models with some fluency. Public programmes reward efficiency and compliance. Private projects reward speed and flexibility. PPPs demand life-cycle thinking and measurable performance over time. Navigating these differences is becoming a core capability.

In the near term, the education construction sector has a solid work bank. Beyond that, the outlook depends on factors that sit partly outside its control. Fiscal tightening could constrain future pipelines. Labour shortages may persist. Procurement systems will be tested.

There is a tendency to look at a figure like $283.5bn and assume momentum will carry through. It might. But pipelines do not deliver projects. People, systems and decisions do. At present, all three are under pressure.

This article is based on an extract of education construction projects pipeline data and commentary provided by GlobalData. Figures and examples cited are attributed to GlobalData’s education project pipeline insights.

To access the full report, visit the GlobalData Construction Intelligence Centre: www.globaldata.com/industries/construction.